With rising multifamily deliveries, an uncertain macroeconomic environment, and volatile interest rates, determining your next step when faced with maturing construction debt or financing your lease-up property is not always clear. With increasing liquidity and growing flexibility in financing options, the lease-up market has entered a dynamic new phase. Against the backdrop of elevated supply weighing on fundamentals, Walker & Dunlop experts recently discussed the evolving environment, offering actionable insights for owners, sponsors, developers, and investors. Here’s what’s shaping today’s market—and where the opportunity lies.

The role of advisory: think multi-track, not one-track

Given credit liquidity, supply trends, investor demand, and agency appetite, multifamily property owners shouldn’t default to a single strategy. The savviest operators are evaluating multiple executions simultaneously, including agency takeouts, bridge debt, recapitalizations, and sales, to preserve flexibility and allow them to respond quickly as market conditions evolve.

Execution flexibility is a strategic advantage. The most successful owners engage advisors who have deep knowledge of the capital markets and can advise them on debt, equity, and sales executions concurrently—making real-time decisions based on the best economics available. Without the right partner to guide them, people are often unaware of how much optionality they have. Walker & Dunlop’s platform is built to support this multi-track strategy, integrating capital markets, agency financing, and investment sales.

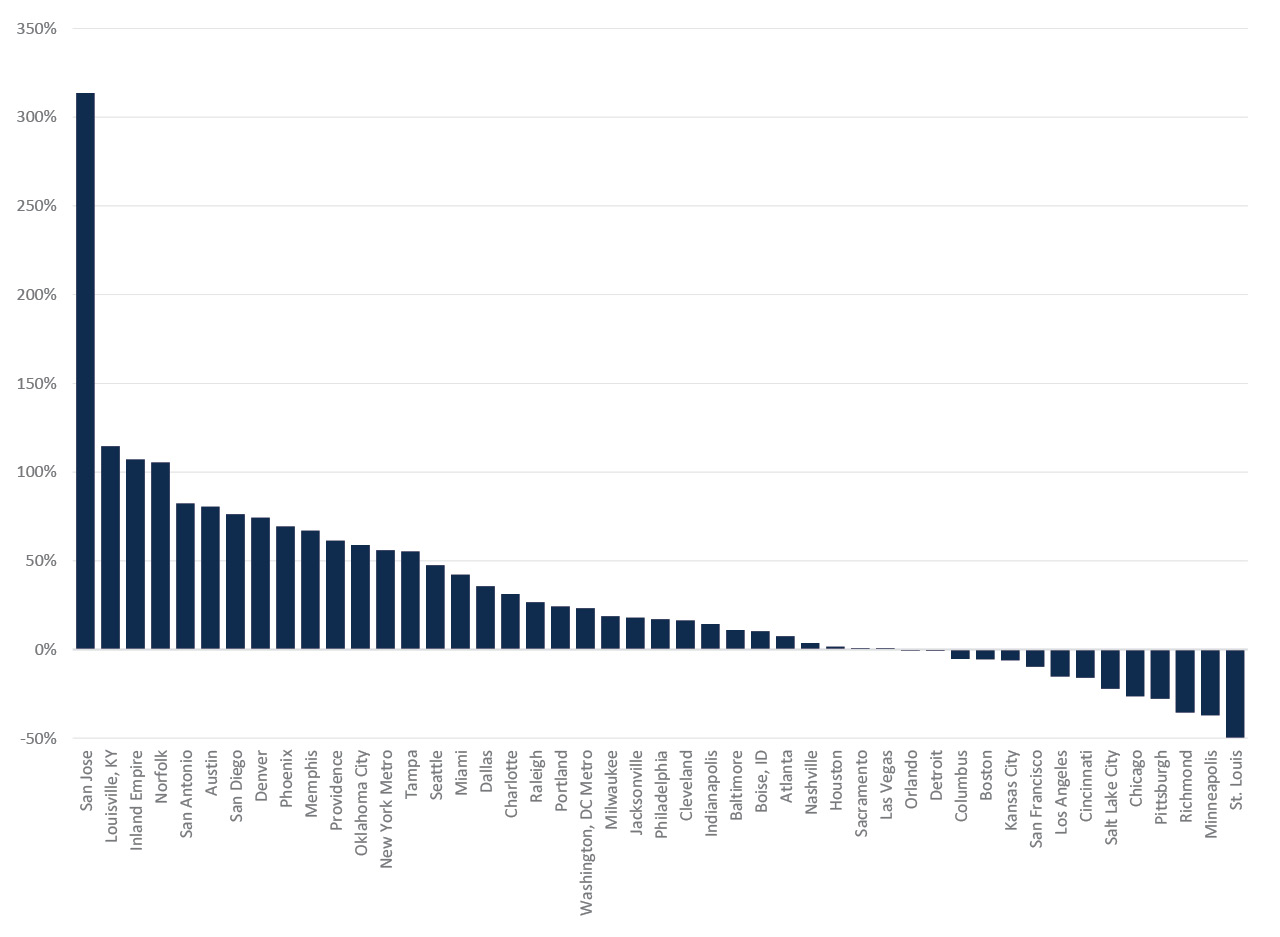

Setting the stage: Today’s multifamily supply picture shows deliveries are peaking but remain historically elevated

Apartment Deliveries in the Trailing 12 Months, Year-over-Year Change %

Data includes the 47 “primary” markets, which are markets that have at least 100,000 units of apartment inventory.

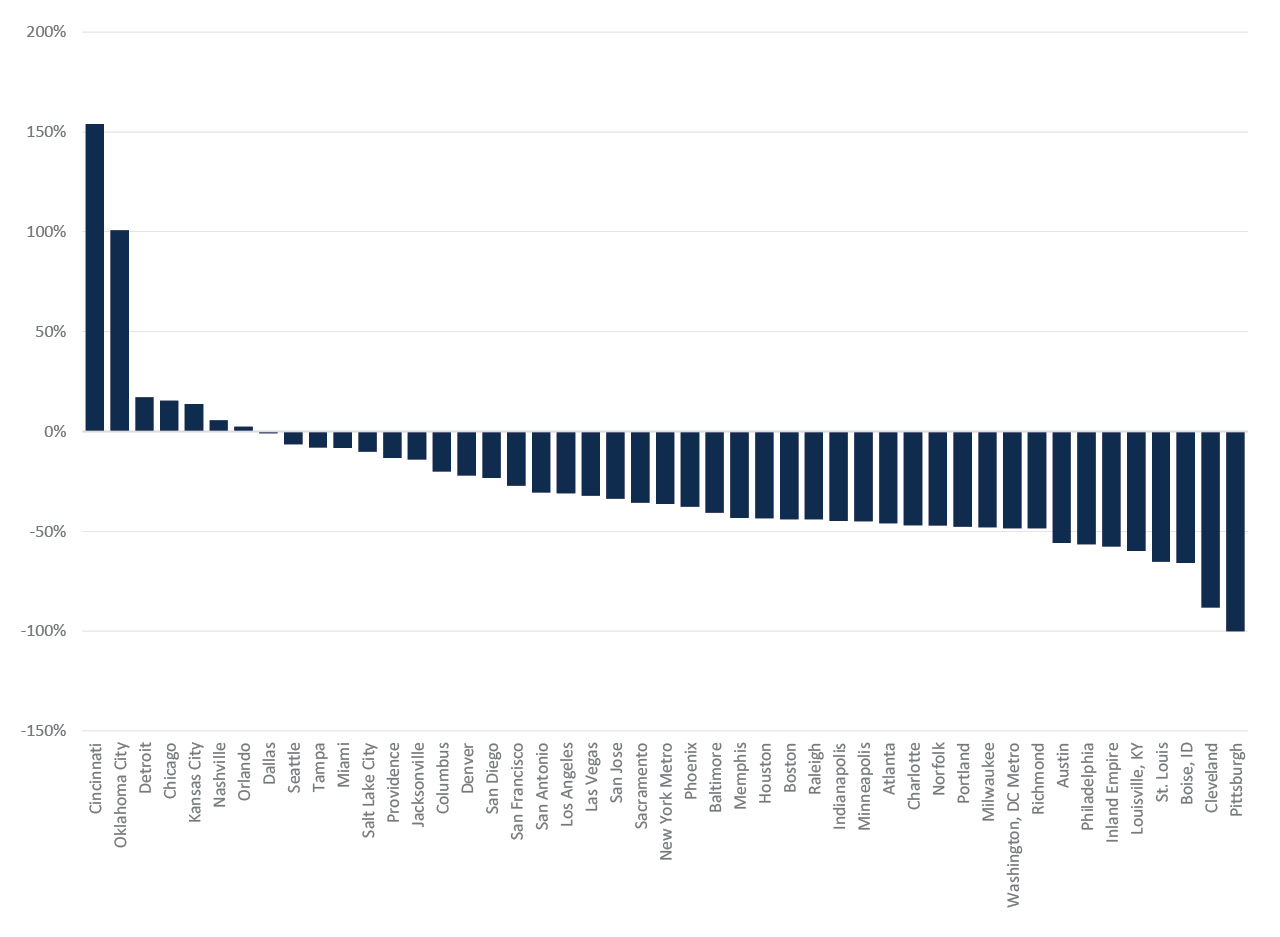

Apartment Deliveries in the Trailing 12 Months Compared to the Average Year Between 2012-2019

Zelman tracked 54 markets to determine the ratio of deliveries over the last 12 months compared to pre-pandemic.

As illustrated by these two charts, Zelman data shows a strong pipeline of multifamily deliveries in key markets with year-over-year increases from 2024. While deliveries are expected to decline in 2025 for many of the tracked markets, they remain significantly above the 2012–2019 historical average; for 25 of the 54 tracked markets, 2025 deliveries are at least 2x pre-pandemic levels. Phoenix, for example, delivered 5,500 units per year on average from 2012-2019 and is expected to deliver 27,000 units this year. This context is essential: 2024 may have been the peak, but elevated delivery levels still impact fundamentals across most primary markets.

Fewer construction starts set the stage for a turning point in lease-up fundamentals

Apartment Construction Starts in the Trailing 12 Months, Year-over-Year Change %

It includes the 47 “primary” markets, which are markets that have at least 100,000 units of primary inventory.

Although 2025 deliveries are elevated, construction saw a meaningful decrease year-over-year. Only 6 of the 54 markets showed an increase in multifamily starts in 2024, while most markets showed double-digit decreases. The debate continues on how far starts may fall in 2025 and beyond, but the trend signals a future tightening of new supply and reduced competition in the years ahead and in high-barrier metros where construction starts pulled back earlier, investors are already anticipating long-term rent recovery potential and are actively pursuing lease-up assets. W&D also expects the tapering of supply to ease downward pressure on lease-up absorption perhaps as early as 2026. All of this bodes well for owners holding or recapitalizing now.

Rent growth varies—highlighting market-specific strategy

Year-over-Year Same Store Effective Rent Growth % as of July 2025

It includes the 47 “primary” markets, which are markets that have at least 100,000 units of primary inventory.

Rent growth as of Q4 2024 varied widely across markets, with 31 markets showing positive year-over-year growth and 23 markets experiencing negative trends.

Muted national rent growth is tied directly to peak lease-up competition. As new deliveries slow and absorption catches up, growth may resume, but performance will remain highly regionalized. The data supports cautious optimism. While absorption challenges exist, many markets continue to outperform expectations. The key is to know your market and to tailor lease-up strategy to local rent dynamics, absorption trends, and competitive set. Supply is coming into the market, but some markets are recovering faster than others, so deep market knowledge is key.

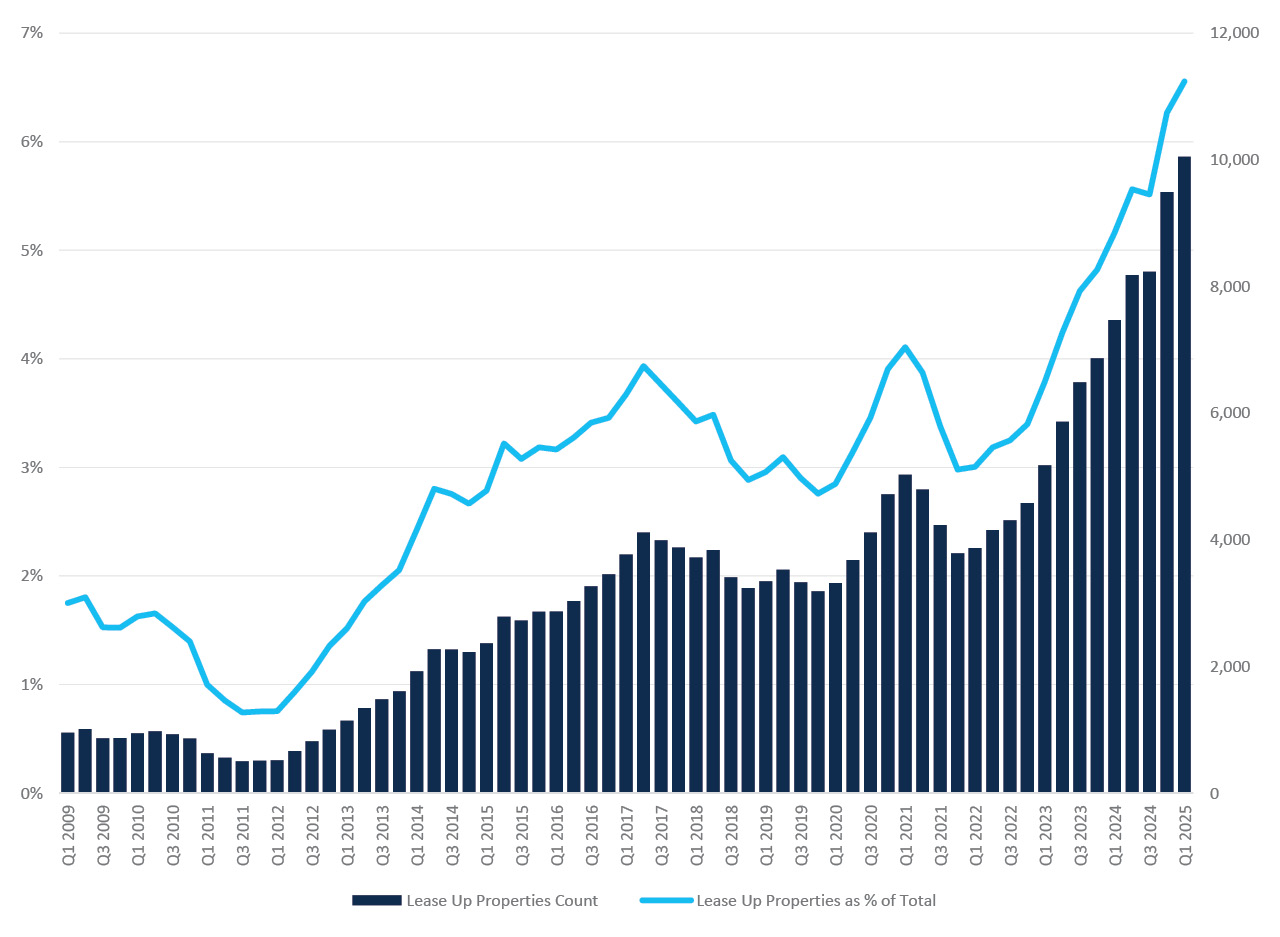

Lease-up competition is at a high point

Total Apartment Properties across the U.S, in Lease Up and as % of the Market

Lease-up properties are currently at peak levels—both in total count and as a percentage of all apartment communities nationwide. This makes for a hyper-competitive leasing environment.

Muted rent growth and longer stabilization timelines are a natural result. The good news? As deliveries fall, lease-up competition should follow suit.

Timing matters. Conditions are challenging now, but are expected to improve as pipeline pressure eases.

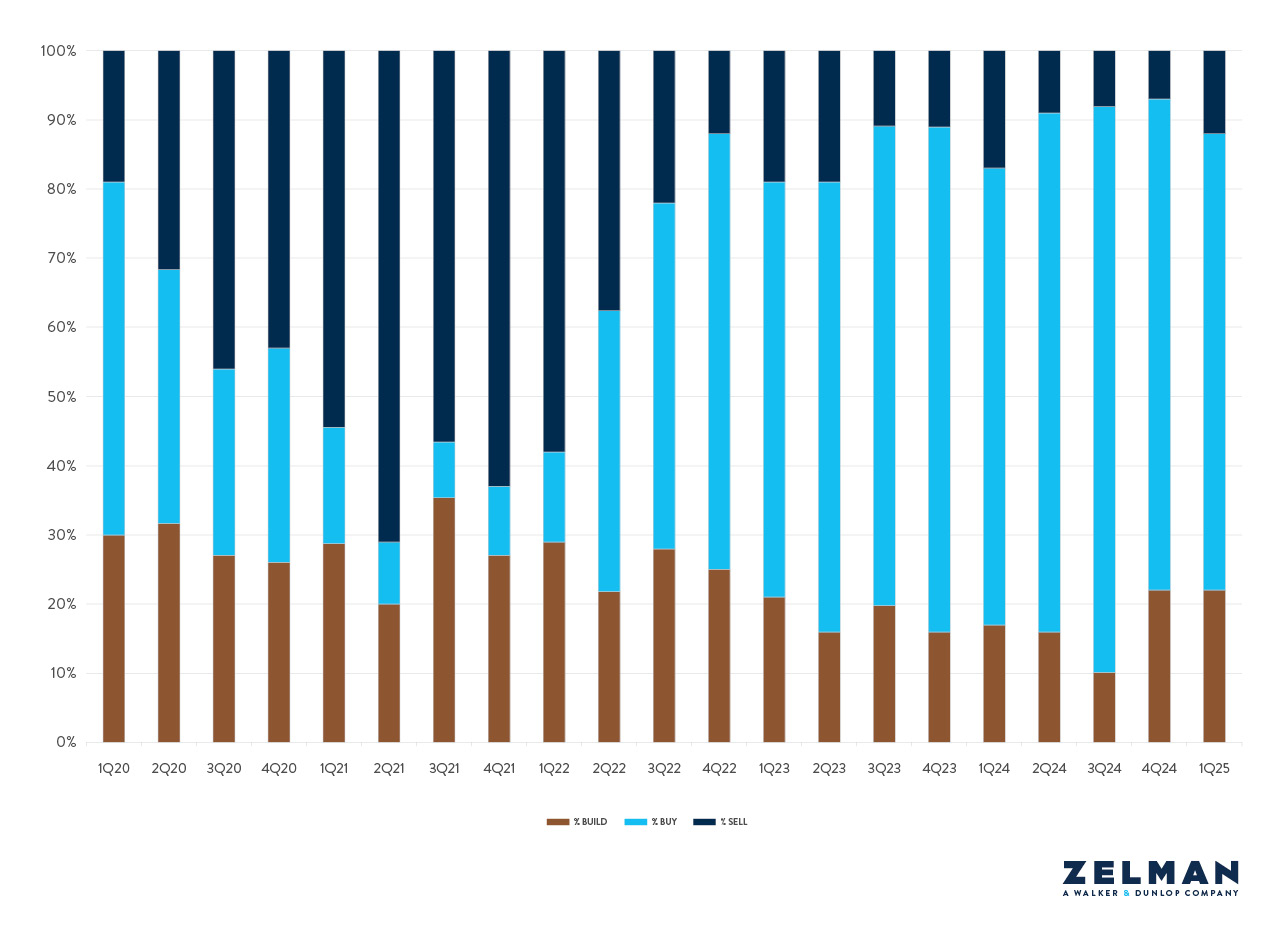

In today’s multifamily environment, is the superior opportunity to build, buy, or sell?

Zelman’s Apartment Transaction Survey asks our extensive network of multifamily owners, operators, developers, and brokers what they see as the best investment opportunity given current market trends. Since 2013, buy is currently near its all-time high and sell is near all-time lows, while build is gaining steam. More appetite to buy and less appetite to sell, however, leads to a disconnect in the market, driving more uncertainty.

Weighing your options in this macro environment

For owners, the current market dynamics signal a strategic inflection point. With buying appetite strong and selling sentiment low, capital remains eager to deploy. However, owners do not necessarily believe that current pricing is reflective of long-term fundamental value and may not be eager to transact under these conditions. This creates a window where refinancing may be a smart move for some, but not the only play. Owners with stabilized assets might still benefit from a sale if they can capitalize on demand in submarkets with strong fundamentals or unlock portfolio-level premiums. At Walker & Dunlop, we’re advising clients to assess all options—refinancing, recapitalization, or strategic sale—based on their long-term goals and asset performance, not just the market headlines.

Capital markets are wide open—especially in lease-up

Liquidity in the capital markets continues to surge, with plentiful floating-rate debt and creative short and long-term fixed-rate options. Lenders are showing strong interest in recently constructed properties and becoming increasingly aggressive, with some willing to refinance construction loans even before a certificate of occupancy (CO) is secured. This increase in availability is driving competitiveness in the debt markets; Walker & Dunlop sees this momentum as a signal for property owners to evaluate their construction take-out strategy early.

Bridge lenders and debt funds are highly active. For well-sponsored projects, capital is more accessible than ever—especially during lease-up. The current state of the market provides an opportunity to refinance expensive construction debt and lock in favorable financing during the lease-up period and beyond.

Agencies offer tailored solutions for pre-stabilized assets. Fannie Mae and Freddie Mac are growing more competitive in the lease-up financing space, trying to lock in permanent debt (and lock out other lenders) earlier in the process. Recent changes in underwriting criteria reflect a willingness to engage in financing discussions earlier in the asset lifecycle, with rate locks as early as 50 percent occupancy and closing at 75 percent. While both agencies remain selective, sponsorship quality remains a key differentiator, with the agencies evaluating assets and prioritizing sponsors with proven track records. This makes a strong operator reputation more important than ever when pursuing early-stage agency execution.

Walker & Dunlop recently released an article describing these changes, Understanding construction loan takeout options: Fannie Mae Near-Stabilization vs Freddie Mac Lease-Up, and how to take advantage of the agency lease-up programs.

Investors are ready to deploy

There’s strong investor interest in acquiring lease-up assets, especially as valuations adjust and opportunities arise. In specific markets with improving fundamentals, lower or decreasing supply, and/or long-term demographic tailwinds, competition is stiff and bid sheets are deep, allowing owners to exit now at favorable pricing, especially as compared to a year ago. In these circumstances, capital that has been sitting on the sidelines is willing to underwrite through negative leverage to the other side of the delivery pipeline, seeing today’s market as offering an attractive entry point.

Looking ahead to the future for lease-ups

Optionality is the name of the game. Aligning execution strategies across debt, equity, and disposition channels is critical. In markets where deliveries are peaking but expected to slow in the future, investor appetite is especially strong. Clients evaluating whether to hold, sell, or refinance should consider multiple execution paths simultaneously.

As lease-up dynamics continue to evolve, Walker & Dunlop remains a trusted partner in guiding clients through each phase of the asset lifecycle. Whether you’re seeking capital, preparing for a sale, or navigating the complexities of agency financing, our team brings unmatched market intelligence and execution certainty.

Want to learn more? Connect with our team to discuss your next move in today’s lease-up market.

Trending

Related insights & perspectives

News & Events

Find out what we’re doing by regularly visiting our news & events page.

Walker Webcast

Gain insight on leadership, business, the economy, commercial real estate, and more.