Executive summary

Read time: 12 minutes

Three forces converging

HUD financing enters 2026 in a fundamentally stronger position, and the market is starting to recognize it. After several years of volatility, elevated rates, and constrained development, three forces are converging: meaningful policy changes, measurable improvements in execution, and a capital markets environment that increasingly rewards stability. Together, these forces are transforming HUD from a perceived niche solution into a core component of sophisticated capital strategies.

Economics & execution are improving

The most important shift is operational. HUD is becoming faster, more predictable, and easier to execute. Processing timelines have compressed materially, internal workflows are improving, and underwriting is moving toward a more efficient, risk-focused approach. These are not incremental changes; they remove one of the primary barriers that had historically limited HUD adoption.

Policy changes are materially improving loan economics. Adjustments to vacancy assumptions, leverage, and debt service coverage are increasing proceeds and expanding feasibility. The elimination of large loan constraints is opening the door to institutional-scale transactions, accelerating HUD’s move upmarket.

Demand supports momentum

Market conditions are reinforcing this shift. Owners and developers are increasingly prioritizing long-term certainty, higher leverage, and protection from future rate volatility. Refinancing demand is building as loans mature and owners transition away from short-term structures. Development remains constrained, but targeted policy changes, particularly around middle-income housing, are helping many deals pencil again.

What this outlook covers

HUD’s operational transformation and faster, more predictable execution

Policy changes improving loan economics, leverage, and scalability

Capital markets dynamics and HUD’s growing role in a selective lending environment

Demand fundamentals, including the expansion into workforce and middle-income housing

Development constraints and how HUD is improving project feasibility

Regulatory and macro factors shaping execution, risk, and program evolution

Strategic opportunities for borrowers leveraging HUD for stability and long-term financing

Market fundamentals

The fundamentals entering 2026 are defined by imbalance and opportunity.

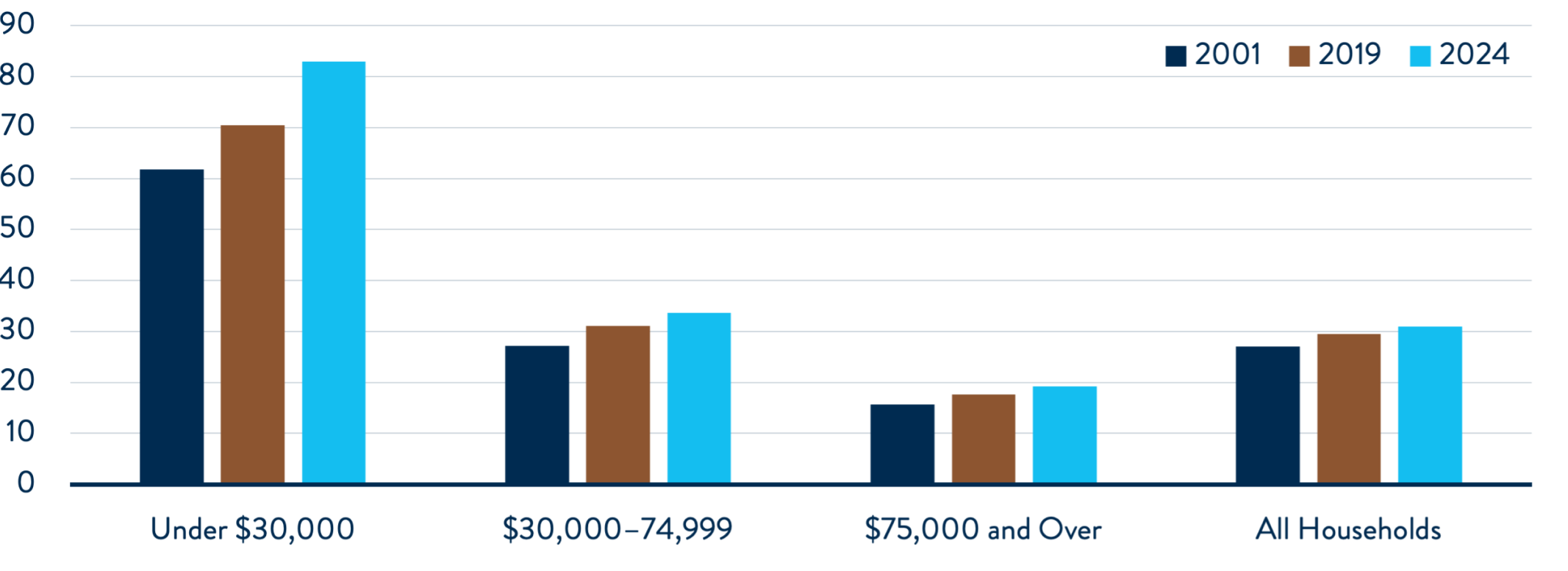

Demand for rental housing remains durable, but affordability constraints are intensifying. The most significant pressure point is not at the lowest end of the market, but in the middle. A growing share of renters earns too much to qualify for traditional affordable housing yet cannot sustainably afford market-rate rents.

HUD’s expansion into workforce and middle-income housing directly addresses this gap.

Housing Has Consumed a Growing Share of Renters' Income

Median Share of Income Spent on Rent and Utilities (PERCENT)

Notes: Non-cash renters are excluded. Households incomes are adjusted for inflation using the CPI-U for All Items.

Shares are calculated at the household levels.

Source: JCHS tabulations of US Census Bureau, American Community Survey 1-Year Estimates.

By supporting units at up to 120 percent of the area median income, HUD is no longer confined to a narrow affordability band. It is now aligned with one of the largest and fastest-growing demand segments.

Geographically, activity continues to concentrate in the Southeast, Southwest, and other secondary and tertiary markets. These regions offer a combination of population growth, relative affordability, and favorable underwriting dynamics. Even in previously oversupplied markets, absorption is improving and select opportunities are re-emerging.

At the same time, operating realities have shifted. Rent growth has stabilized, while expenses remain elevated. This is forcing more disciplined underwriting and increasing the importance of capital structure in determining whether a deal is viable.

SOUTHWEST FY 2023- 2025 Spotlight

SOUTHEAST FY 2023- 2025 Spotlight

Capital markets overview

The capital markets environment is stabilizing but not easing.

Interest rates have moderated, but capital remains selective, and underwriting standards remain disciplined. Borrowers are still facing a higher cost of capital than in prior cycles, and that reality is reshaping financing decisions.

In this environment, HUD is gaining ground.

With the recent introduction of more than 20 proposed policy changes in a draft mortgagee letter, execution is materially improving. These improvements include:

- Reduction in vacancy assumptions to better reflect market realities

- Improvement in proceeds due to lower debt service requirements

- Higher leverage, particularly for middle-income housing

- Removal of large loan constraints enabling institutional deals

This is a meaningful shift. HUD is no longer just competing on structure; it is competing on economics.

Stay updated on market insights

Subscribe to receive the latest news, insights, and future Outlook releases from Walker & Dunlop.

How HUD compares

ConstructIon debt

HUD vs. Life Insurance Co. vs. Bank

refinance

HUD vs. GSE

HUD’s core advantages remain unchanged: long-term, fixed-rate, non-recourse financing with high leverage and construction-to-permanent execution that eliminates the conversion or lease-up risk associated with insurance and bank construction financing. In a market where capital availability can shift quickly, those characteristics are increasingly valuable.

Development & supply pipeline trends

Construction costs remain elevated, labor constraints persist, and regulatory factors continue to affect feasibility. Many projects still require higher equity contributions than in prior cycles, limiting new starts.

Construction spending

(Seasonally Adjusted Annual Rate (SAAR)) Billions of dollars

Source: U.S. Census Bureau, March 23, 2026

However, conditions are improving at the margin, and HUD is a key driver of that improvement.

One of the clearest signals is the return of full-cost financing, which reflects a broader shift:

- Lower equity requirements

- Improved deal viability

- Increasing developer confidence

HUD’s structure is also changing how developers think about capital strategy. Rather than relying on interim financing and hoping for improved exit conditions, they are increasingly seeking permanent solutions earlier in the lifecycle.

Middle-income policy changes are unlocking projects that previously did not pencil by improving leverage and lowering debt service requirements.

In sectors such as seniors housing, the story is different. Demand is growing, but new supply remains limited due to cost constraints. As a result, activity is shifting toward rehabilitation and repositioning rather than new construction. The development pipeline is not expanding rapidly, but it is becoming more executable.

Policy, regulatory, & macro considerations

HUD’s evolution is being driven by a coordinated push across execution, policy, and regulation.

Efforts to streamline execution are already underway, with improvements in underwriting processes helping reduce timelines and increase predictability. With the introduction of the Lean Express loan, Lean closing reforms are also underway, with changes being rolled out in stages. The reforms include evaluating which exhibits are truly necessary, standardizing punch lists, and clarifying roles and responsibilities among stakeholders to drive greater consistency at closing.

HUD’s latest mortgagee letter signals a proactive approach to modernization, including adjustments to underwriting standards and expanded program flexibility.

HUD has scaled back several restrictive environmental policies to reduce transaction costs, improve processing timelines, and increase certainty of execution for FHA multifamily financing. By aligning environmental diligence more closely with actual loan risk, the new guidelines create a more predictable and efficient path for borrowers seeking FHA-insured capital while supporting the delivery of housing.

The changes narrow HUD’s environmental review to better align with other financing sources. Key updates would include reinstating prior guidance on buried pipelines and fall hazards, limiting noise analysis to relevant property uses, and reducing requirements related to high-voltage transmission lines and vibration. Together, these changes eliminate unnecessary third-party reports, lower costs, and improve deal certainty while maintaining sound underwriting standards.

Additional policy considerations include:

- Allowing 5 percent vacancy underwriting on 223(f) transactions

- Eliminating large loan requirements

- Reducing certain technical reviews

- Modernizing select documentation requirements

Promoting modular construction is another area of policy. By encouraging construction methods that can reduce timelines and increase cost predictability, HUD is signaling support for innovation that will help builders meet affordability goals. Faster delivery and lower construction risk directly support feasibility in today’s cost environment.

HUD is considering allowing both new construction and recently constructed (less than three years old) purpose-built rental projects to qualify under revised build-to-rent (BTR) guidance. Importantly, projects would no longer need to meet the prior 50 percent four-unit structure threshold, provided they are designed and built for rental use and offer market-consistent amenities.

Regulatory considerations remain a key factor in construction feasibility, particularly around labor costs. Davis-Bacon wage requirements remain in place, but discussions are focused on common-sense adjustments that reflect current market realities. Similarly, HUD is evaluating elements of the National Environmental Policy Act (NEPA) implementation framework and advancing modernization efforts around environmental reviews, noise calculations, and Choice Limiting Actions.

Broader macro conditions also continue to influence HUD’s trajectory. Interest rates, inflation, and federal budget priorities will shape risk tolerance and program expansion. For now, the environment appears supportive of continued evolution.

Outlook & strategic opportunities

Looking ahead, HUD’s role in the commercial real estate finance ecosystem is poised to expand.

Refinancing activity is expected to increase as owners address upcoming maturities and seek long-term stability. At the same time, HUD’s flexibility is enabling increasingly complex transactions.

Middle-income housing represents one of the most significant opportunities in the market, addressing a critical gap between traditional affordable housing and market-rate development. HUD is also reinforcing its role as a countercyclical solution. In periods of uncertainty, its long-term, fixed-rate structure provides stability and predictability that many other capital sources cannot match.

Complexity will also increase. Transactions will require more structuring, more creativity, and deeper expertise.

Valuations will remain a critical control point for clients with greater importance placed on clear, well-supported analysis that is documented in the appraisals. Market studies should directly address asset- and market-level risks and mitigants, with thoughtful discussion of capture, absorption, vacancy, concessions, and other demand indicators that influence underwriting.

However, conditions are improving at the margin, and HUD is a key driver of that improvement.

One of the clearest signals is the return of full-cost financing, which reflects a broader shift:

- Lower equity requirements

- Improved deal viability

- Increasing developer confidence

HUD’s structure is also changing how developers think about capital strategy. Rather than relying on interim financing and hoping for improved exit conditions, they are increasingly seeking permanent solutions earlier in the lifecycle.

Middle-income policy changes are unlocking projects that previously did not pencil by improving leverage and lowering debt service requirements.

In sectors such as seniors housing, the story is different. Demand is growing, but new supply remains limited due to cost constraints. As a result, activity is shifting toward rehabilitation and repositioning rather than new construction. The development pipeline is not expanding rapidly, but it is becoming more executable.

Special thanks to:

Nelson Pratt, Jason Silva, Mike Valucci, Kim Miles, Carson Petraitis, Taylor Thompson, Matt Mentesana, Alex Luzzaraga, Parker Kent, Johnny Rice, Carrie Chrismer